Myanmar, also known as Burma, is often portrayed internationally as a country defined by collapse since the 2021 coup, weakened by military rule, civil wars, sanctions, and institutional breakdown. Yet this dominant narrative conceals a more consequential reality. Quietly and with limited global attention, Myanmar has become China’s largest external supplier of raw heavy rare-earth elements (REEs). Almost all of Myanmar’s rare-earth exports go directly to China, while China controls more than 90 per cent of global refining and

processing capacity for high-value heavy rare-earth components in the global supply change.

Despite this structural importance, Myanmar’s leverage remains constrained by political instability and fragmented governance, dependence on a single dominant downstream buyer, the absence of refinery technology, and the lack of a coordinated resource management system. As a result, it captures only limited economic and strategic advantages from the resources it controls. Myanmar’s exports to China reached approximately USD 4.3 billion in cumulative value between 2017 and 2025. In 2025 alone, rare-earth exports totalled more than USD 624 million, representing over 28,000 tonnes.

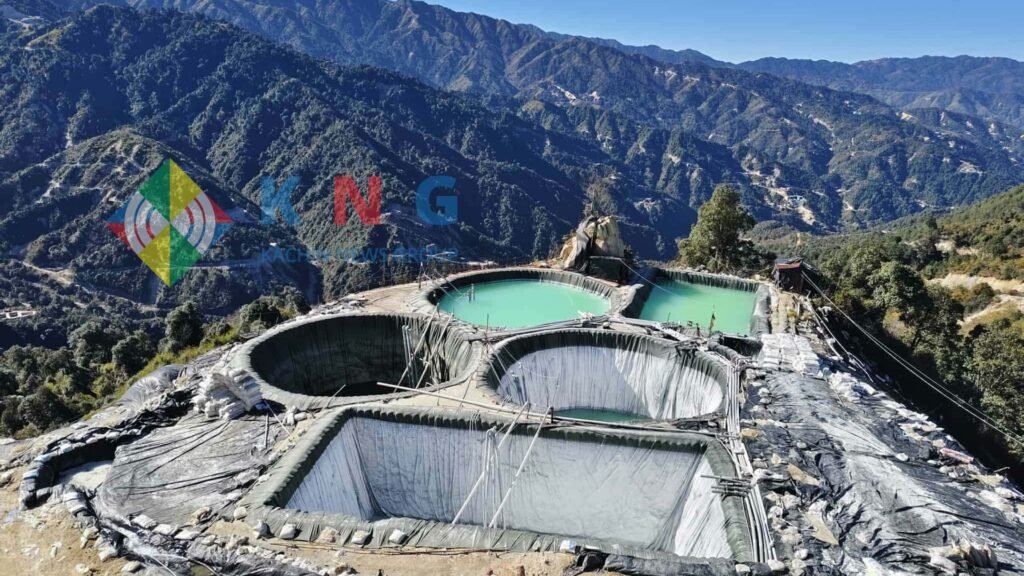

At the centre of this development lies the Kachin State. The global energy transition depends materially on heavy rare earths such as dysprosium and terbium, key components used in electric vehicles, wind turbines, robotics, and advanced defence technologies. While the global economy speaks confidently about clean energy transitions, digitalisation, and technological innovation, the raw materials sustaining these ambitions are increasingly extracted from Kachin soils in Myanmar, particularly in regions such as Chipwi and Momauk,

under fragile political and environmental conditions.

Here, a supply chain refers to the full journey of a resource from extraction and processing to manufacturing and final distribution. In the global heavy rare-earth supply chain, Myanmar dominates the extraction stage, particularly from ion-adsorption clays concentrated in Kachin State. China dominates global refining, chemical separation, and high-value manufacturing, while most finished rare-earth products are also produced either in China or in industrial economies dependent on Chinese processing capacity.

Extraction of these minerals is not easily replaced. New mining projects in Australia, Africa, or the Americas face lengthy environmental approvals, high investment costs, technological constraints, and community resistance. Recycling technology also remains insufficient to meet growing demand, while substitution options are limited. These structural realities make Kachin’s rare-earth output highly rigid and significant in the short and medium term. However, structural importance alone does not automatically translate into leverage.

Leverage, in this context, refers to the ability to influence pricing, negotiate trade terms for local benefits, shape certain market conditions, and convert resource control into political economic advantages. A major factor weakening this leverage is internal political instability and fragmented governance. Control over rare-earth mining areas in Kachin State has shifted in recent years. The Kachin Independence Organisation (KIO) has consolidated authority over major mining zones in Kachin state previously overseen by the New Democratic Army–Kachin (NDAK), which had been aligned with the Myanmar military. The KIO now administers these areas and secures transportation routes to the China border. Export levies reportedly amount to around 35,000 yuan (approximately USD 4,800) per tonne. Rare-earth governance has therefore become intertwined with borderland political bargaining and power consolidation.

But mining operations largely continue to function within informal regulatory systems. Only a fraction of revenues is captured sub-nationally, while enforcement remains political rather than institutional, and extraction continues under informal arrangements that prioritise immediate revenue over long-term leverage.

But the environmental and social consequences are borne primarily by local communities in Kachin State. Reports of water contamination, deforestation, soil degradation, landslides, and serious health risks, including fatalities, are widespread. Acid-leaching methods used in mining carry significant ecological risks. Workers in these mining areas reportedly earn around USD 800 per month, which remains low compensation for their hazardous labour. Although many local communities strongly oppose these mines due to the environmental damage caused by them, resistance has often been tempered by their political-economic necessity. In the context of prolonged civil wars and limited livelihood options, some local communities have reluctantly tolerated these mining activities in the expectation of securing at least minimal economic returns during this period of severe instability. But residents receive only limited returns proportional to what they contribute, yet they bear the environmental and social costs with little compensation.

International sanctions imposed since the 2021 coup have further complicated the situation. Many major Western actors introduced targeted sanctions on Myanmar military leaders and military-linked enterprises, yet rare-earth extraction networks and cross-border trade have largely continued. Heavy rare-earth flows remain closely tied to Chinese industrial demand and operate through Kachin borderland trade networks. Sanctions have therefore produced a paradox: reduced Western engagement has narrowed external partnerships and

increased reliance on a single downstream buyer.

To strengthen the local supply chain leverage, it must be grounded in pragmatic responses to present realities. Greater transparency in taxation and revenue allocation within existing administrative structures is essential for building public trust and ensuring that resource revenues are allocated. At the same time, developing small pilot-scale domestic processing initiatives could gradually build technical capacity to retain greater value. In addition, cautiously diversifying economic partnerships in rare-earth trade could reduce dependence on a single downstream buyer. Recently, neighbouring India has shown emerging interest in Myanmar’s REE, presenting a potential opportunity to broaden strategic options.

Beyond these structural measures, several immediate steps could strengthen leverage under current governance conditions. First, the local authority can introduce a structured community revenue-sharing mechanism that ensures a defined portion of mining income is directly redistributed to local communities of the mining regions. These funds could support public welfare and education, healthcare services, and environmental rehabilitation in affected communities, ensuring that extraction generates tangible local benefits, rather than concentrating revenue solely within trading networks.

Second, strengthening local worker protections and wage standards within mining operations can also increase local economic benefit capture. Workers in these mining areas currently face hazardous working conditions with limited protection. Policies such as wage standards, safety regulations, and labour representation mechanisms for these mining zones could ensure that a share of resource wealth circulates within local communities rather than leaving the region entirely.

Third, local authorities could improve oversight of mining concessions and licensing practices by limiting the uncontrolled expansion of extraction sites with accountability. Establishing clearer permit systems and operational quotas would help prevent excessive resource depletion while also allowing local authorities to exercise greater control over downstream production levels.

Finally, improving local bargaining capacity also requires strengthening coordination and oversight on how existing payments and trade arrangements are negotiated and implemented. Although Chinese companies currently conduct most extraction activities and provide certain payments through export levies, wages, and land-use arrangements, these negotiations often occur on a fragmented basis. Greater coordination among local authorities and mining operators could strengthen their ability to negotiate more consistent terms and

ensure that the economic benefits of the extraction process are distributed more fairly.

Thus, the quiet loss of supply chain leverage ultimately lies in the lack of opportunity to convert structural indispensability into coordinated economic and political advantage. Local authorities may control extraction, but China continues to dominate refining and downstream industrial integrations. Yet, this leverage is not solely a state-level issue. It also connects directly to public participation and community organisations. Local communities can strengthen their efforts on environmental monitoring, documentation of ecological damage and loss, and collective advocacy for remediation mechanisms. Civil society organisations and diaspora networks also need to conduct more on local awareness, and voice out more to the international community on responsible mineral sourcing and accountability, encouraging manufacturers to adopt environmental and local governance standards in procurement decisions.

Myanmar is a critical part of the material foundation of the global energy transition, and Kachin State bears a disproportionate share of the environmental and social burden. Yet the region remains locked in a low-value, high-risk position within the supply chain it materially sustains. Recognising Myanmar’s strategic position in rare-earth supply chains does not imply endorsing current mining practices or political arrangements, but rather highlights the need for responsible governance and strategic management to leverage this strategic position. Leverage can be grown when communities are informed, coordinated, and able to articulate shared demands.

Therefore, the quiet loss of strategic supply chain leverage is in local governance, coordination, strategic management, and the role of the public. In an era defined by geopolitical competition and energy transformation, leverage belongs not merely to those who control the resource but to those who organise, regulate, and strategically manage what they control. At present, Myanmar does the former while steadily losing the latter.

The views expressed in this guest column are those of the author and do not necessarily reflect the editorial position of Kachin News Group.